Question

I have noticed that calls on the VIX trade at a discount. Why is that? Is there an arbitrage opportunity? What am I missing?

Answer

These days, the financial news is littered with talk about the VIX. It reflects the implied volatility of the SPX (S&P 500 Cash Index) options. To keep things simple, it measures the amount of uncertainty in the marketplace. As the uncertainty increases, the options become more expensive and it costs investors more to buy puts (insure their portfolio). Before I answer the question, let me use the definition from the CBOE to define the index.

Definition – The CBOE Volatility Index – more commonly referred to as “VIX” – is an up-to-the-minute market estimate of expected volatility that is calculated by using real-time S&P 500® Index (SPX) option bid/ask quotes. VIX uses nearby and second nearby options with at least 8 days left to expiration and then weights them to yield a constant, 30-day measure of the expected volatility of the S&P 500 Index.

Expiration date – The Wednesday that is thirty days prior to the third Friday of the calendar month immediately following the expiring month. The following are the expiration dates for VIX options that may be listed through December 2008:

Settlement – The exercise-settlement value for VIX options (Ticker: VRO) shall be a Special Opening Quotation (SOQ) of VIX calculated from the sequence of opening prices of the options used to calculate the index on the settlement date. The opening price for any series in which there is no trade shall be the average of that option’s bid price and ask price as determined at the opening of trading. Exercise will result in delivery of cash on the business day following expiration. The exercise-settlement amount is equal to the difference between the exercise-settlement value and the exercise price of the option, multiplied by $100.

There are three very important characteristics that make this product different from stock options. First of all, the expiration date is not on the third Friday of the month. Traders need to be aware of the expiration cycle. Secondly, the options are European style. That means that the options can be traded, but they can not be exercised before expiration. Finally, the settlement is a cash-based. This means that if the option is in the money when the VIX settles, your account will be credited the intrinsic value of the options.

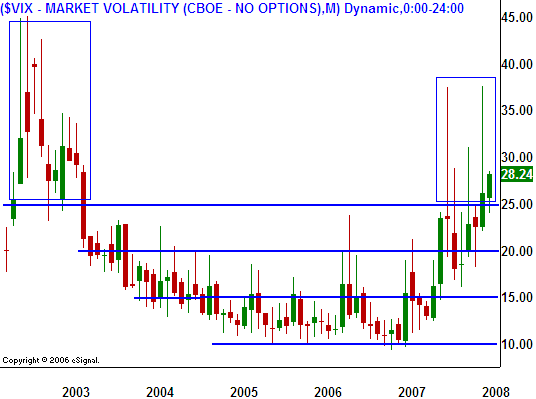

The reason these call options trade below parity (price of VIX less the strike price) can be seen in the chart. In the last seven years, the VIX has had some large spikes above 30, but that price level does not hold for very long. Eventually, the market evaluates new information and it calms down. From a probability standpoint, traders believe that the implied volatilities will drop in the next few months.

.

.

.

.

Since the options can not be exercised early, they can be priced at a discount. A speculator who believes the second shoe has yet to drop, might buy the calls and get a “good deal”, but they are trading against the historical pattern for the index.

If the options were American-style, there would be an arbitrage opportunity. You could purchase the calls at a discount and exercise them for a cash gain. Obviously, this practice would continue until the options trade at parity.

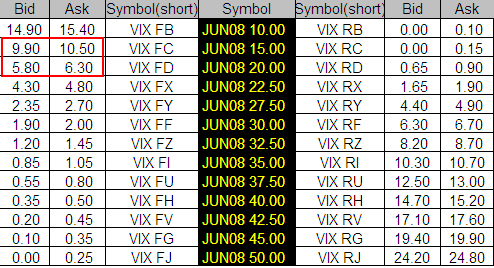

In the option chain, you can see that the June 20 calls are offered at $6.30. As of this writing, the VIX closed at 28.24. Those options are $8.24 in the money and they are trading at a $2.00 discount.

.

.

.

.

There are many articles that are written about the VIX. It is a broad-based measure of uncertainty. Option traders should use this as a gauge and they should be buyers of options when the VIX is low (2005-2006) and sellers of options after the peak has been established (August 2007).

This can be a very frustrating product to trade. After the sharp market decline in March 2007, I waited for a snap back rally. I felt that the implied volatility would increase over the next six months and I bought the November 12 calls for $3.10. They traded at a premium and the index was at 12. By mid summer, the volatility picked up and the VIX went up to 16. At that stage I still had not made any money because the options were trading at a discount. The index had moved 4 points (25%) and I was barely profitable. Traders believed that the spike was temporary and the premiums would decline since the VIX had been at historic lows the prior two years.

It wasn’t until the index popped to 20 that I was able to realize a nice profit on the trade. Given the wide bid/ask spread, unpredictable movement and unique settlement, I would not advise you to trade this product. However, these shortcomings do not diminish its value as an indicator.